The Role of Variants in the Vape Market Explained

The Role of Variants in the Vape Market Explained

Product variants, specifically flavors and device configurations, define the role of variants in the vape market by determining who buys, what they buy, and how often they return. Flavor categories like fruit, candy, and dessert drive initiation and repeat purchases. Device types, from disposables to high-capacity multi-flavor pods, shape satisfaction and biological impact. The industry’s growth trajectory, its regulatory battles, and its retail economics all trace back to one core variable: which variants are available and to whom. This article breaks down the data, the trends, and the practical implications for both enthusiasts and analysts.

How do vape product variants influence consumer preferences?

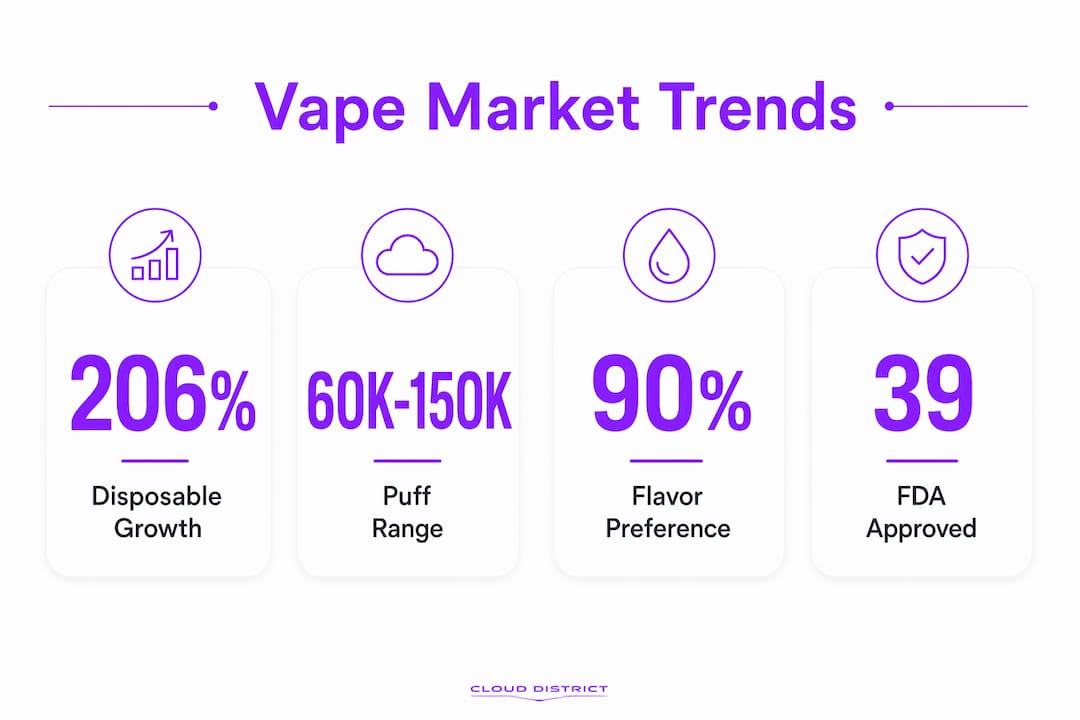

Flavor is the primary driver of consumer choice in the vaping category. Nearly 90% of young users cite flavor as the reason they started vaping. That figure is not incidental. It means flavor functions as the market’s entry mechanism, not just a product attribute.

The most popular flavor categories follow a clear hierarchy: fruit, candy, and dessert profiles dominate among youth and young adults. 97.7% of youth who vaped in 2024 used flavored products, as did 95.5% of young adults. These numbers confirm that unflavored vaping is effectively a niche, not a mainstream behavior.

Device type compounds the flavor effect. Disposables offer zero setup and immediate flavor access, which makes them the preferred format for new users. Multi-flavor devices, which allow users to switch between two or more flavor tanks within a single unit, address the preference for variety without requiring multiple hardware purchases. Consumer demand has shifted toward convenience and variety, pushing manufacturers to design devices that address both preferences simultaneously.

The biological dimension of variant choice is less discussed but equally significant. Gene expression changes in vapers are 66.6% linked to specific flavors and device types, with fruit flavors alone connected to changes in 31% of affected genes. This means the variant a consumer selects is not just a preference decision. It carries measurable physiological consequences that regulators and manufacturers cannot ignore.

Key flavor-driven consumer behaviors include:

- Fruit profiles (strawberry, mango, watermelon) generate the highest repeat purchase rates across both disposable and pod formats.

- Menthol and ice-finished flavors retain strong adult consumer loyalty, particularly among former smokers transitioning from combustible cigarettes.

- Candy and dessert variants show the highest initiation rates among users under 25.

- Tobacco flavors remain the baseline for FDA-authorized products but represent a shrinking share of actual consumer purchases.

Pro Tip: If you are evaluating a new device, cross-reference the flavor profile with the device’s coil resistance. Lower-resistance coils amplify sweetness in fruit profiles, while higher-resistance coils preserve the sharpness of menthol and ice variants.

What market trends emerge from vape product variants?

Disposable vape sales surged 206% between 2020 and 2024, a growth rate directly attributable to flavored variants. That kind of acceleration does not happen from device innovation alone. Flavor accessibility and pricing made high-nicotine flavored disposables the fastest-growing segment in the entire nicotine category.

The shift toward high-capacity devices is the most significant structural trend in 2026. Devices now offer 60,000 to 150,000 puffs with multiple independent flavor tanks. This is not simply a convenience upgrade. It is a strategic product architecture that allows consumers to access flavor variety while manufacturers navigate pod-specific regulations and taxes.

| Market Trend | Driver | Retail Implication |

|---|---|---|

| Disposable sales growth (206% 2020–2024) | Fruit and candy flavor accessibility | High turnover SKUs require consistent restocking |

| Multi-flavor, high-capacity devices | Consumer demand for variety and regulatory pressure | Fewer SKUs needed; higher per-unit margin |

| Pricing compression on flavored disposables | Manufacturing scale and gray-market competition | Price-sensitive consumers shift to value-tier flavored units |

| Flavor curation over broad assortment | Retailer “flavor logic” reducing dead inventory | Disciplined SKU selection improves sell-through rates |

Retailers who stock the widest possible flavor range do not outperform those who curate. Flavor logic, the practice of selecting fruit-led and ice-finished profiles over comprehensive assortments, increases sell-through and reduces dead inventory. The data supports discipline over breadth. A store carrying 40 flavor SKUs with 60% sell-through underperforms one carrying 18 SKUs with 90% sell-through on every metric that matters: margin, cash flow, and shelf efficiency.

Understanding how flavor variants drive foot traffic is equally relevant for operators building loyalty programs and repeat-purchase incentives.

How do regulations interact with vape product variants?

Regulatory policy and variant availability are directly linked. The FDA has authorized only 39 vaping products, the majority of which are tobacco or menthol flavors. Most fruit and sweet-flavored devices remain unauthorized because of documented youth appeal concerns. The agency’s recent approvals of “Sapphire” and “Gold” as fruit-flavored products represent incremental movement, but the authorization pipeline remains narrow relative to market demand.

Local flavor bans produce measurable public health outcomes. Studies of 2.8 million student tobacco users show that local flavored tobacco bans correspond with a 9.3 percentage point lower rate of youth electronic nicotine delivery system use four years after implementation. That is a statistically significant reduction, and it explains why municipal and state-level flavor restrictions continue to expand despite industry opposition.

The public health debate centers on a genuine tension:

- Flavored products help adult smokers transition away from combustible cigarettes, which carry higher mortality risk.

- The same flavors drive youth initiation at rates that create new nicotine dependence in populations that would otherwise not have used any tobacco product.

- FDA authorization processes are slow relative to product innovation cycles, leaving most of the market in a regulatory gray zone.

- Smart vape features, including digital screens and embedded games, compound the youth appeal problem beyond flavor alone.

“Nearly one-third of youth e-cigarette users used ‘smart’ vapes in the past 30 days in 2024, with 32.3% reporting smart vape use that combines flavors with interactive technology to increase engagement among younger users.”

The co-use pattern adds another layer of concern. 45.5% of youth e-cigarette users reported using at least one additional tobacco product. Flavor variety across product categories, from disposable vapes to oral nicotine pouches, creates a multi-product nicotine ecosystem that increases dependence risk beyond what any single variant analysis captures.

What can retailers and manufacturers learn from variant data?

The practical lessons from variant performance data are specific and actionable for anyone managing product assortment or marketing strategy.

Flavor curation outperforms flavor maximalism. Retailers who apply a disciplined flavor logic approach, prioritizing fruit-led profiles with ice-finished options as secondary, consistently achieve better sell-through than those who stock every available SKU. The flavor curation principle is not about limiting consumer choice. It is about matching inventory to demonstrated demand patterns rather than speculative variety.

Key lessons for retail and product strategy:

- Lead with fruit profiles. Strawberry, mango, and watermelon variants generate the highest volume across disposable formats. These should anchor any flavor assortment.

- Use ice-finished variants as secondary anchors. Menthol and ice profiles retain adult consumers and complement fruit-forward selections without cannibalizing them.

- Prioritize high-capacity devices. Multi-flavor units with 50,000 or more puffs reduce the need for multiple SKUs while delivering the variety consumers want from a single purchase.

- Monitor regulatory developments by region. Flavor bans at the local level create abrupt demand shifts. Retailers in jurisdictions with pending flavor legislation should reduce flavored inventory depth and increase tobacco and menthol stock as a hedge.

- Use sales velocity data, not intuition. The variants that sell fastest in one market may underperform in another. Point-of-sale data from systems designed for vape retail operations provides the granular velocity tracking needed to make these calls accurately.

Pro Tip: When introducing a new flavor SKU, run it alongside your top-performing variant for 30 days before committing to full inventory depth. Comparative velocity data from that window predicts long-term sell-through more reliably than supplier projections.

Manufacturers face a parallel challenge. High-capacity multi-flavor devices are a direct response to regulatory pressure on pod-specific products. The strategic design logic behind these devices, which bypass pod restrictions through integrated tank architecture, reflects how product variant development now operates as much in response to regulation as to consumer preference. Understanding disposable vape mechanics helps both consumers and retailers evaluate which device formats offer the best combination of flavor performance and compliance stability.

Key takeaways

Product variants, particularly flavors and device configurations, are the single most influential variable in vape market growth, consumer behavior, and regulatory conflict.

| Point | Details |

|---|---|

| Flavor drives initiation | Nearly 90% of young users cite flavor as their reason for starting to vape. |

| Disposable growth is flavor-led | Disposable sales grew 206% from 2020 to 2024, driven by fruit, candy, and dessert variants. |

| Flavor bans reduce youth use | Local flavor bans correlate with a 9.3 percentage point drop in youth vaping four years post-implementation. |

| Curation beats breadth in retail | Disciplined flavor logic with fruit-led and ice-finished profiles improves sell-through and reduces dead inventory. |

| Device design responds to regulation | High-capacity multi-flavor devices are engineered to deliver variety while navigating pod-specific restrictions. |

Why variant strategy will define the next five years

I have watched the vape market cycle through hardware innovation phases before, and each time the industry assumed device technology would be the primary differentiator. It never was. Flavor is the variable that moves consumers, and the data from 2024 and 2025 confirms this with more precision than any previous cycle.

What concerns me about the current moment is the gap between what the market produces and what regulators can process. The FDA’s authorization pipeline is structurally too slow for an industry that launches new flavor variants monthly. That gap creates a market where most products operate without formal authorization, which is not a stable foundation for long-term industry legitimacy.

The retailers and manufacturers who will be positioned well in five years are those who treat flavor curation as a strategic discipline rather than a sales tactic. Stocking every flavor that ships is not a consumer service. It is inventory risk dressed up as variety. The operators I respect most are the ones who read sell-through data weekly and cut underperforming variants before they become dead stock.

The public health tension around youth-appealing flavors is real and will not resolve itself through industry self-regulation alone. Responsible variant development means designing products and marketing strategies that serve adult consumers without functioning as youth recruitment tools. That is a harder line to hold than it sounds, especially when smart vape features and candy profiles generate the highest short-term sales numbers.

Long-term market sustainability requires the industry to accept that some variants will be restricted, and to compete on the quality and compliance of what remains available rather than on volume and variety alone.

— Justin

Explore top flavor variants at Cloud District

Cloud District carries the flavor variants that consistently lead in consumer preference and sell-through data. The Pulse Strawberry Kiwi Thermal Edition and Pulse Strawberry Mango represent the fruit-forward profiles that drive the highest repeat purchase rates in the disposable category. For consumers who want high-capacity performance with a clean mint profile, the VUE 50K Kit in Miami Mint delivers 50,000 puffs with consistent flavor output. Every purchase at Cloud District earns Cloudz rewards, and local pickup keeps your order fast and straightforward.

FAQ

What is the role of variants in the vape market?

Variants, primarily flavors and device types, determine consumer initiation, satisfaction, and repeat purchase behavior. They also drive regulatory responses and retail stocking strategies across the entire vaping category.

Why do fruit flavors dominate vape sales?

Fruit profiles generate the highest consumer demand across both disposable and pod formats. Nearly 90% of young users cite flavor as their primary reason for starting to vape, with fruit variants leading initiation rates.

How do flavor bans affect the vape market?

Local flavored tobacco bans correspond with a 9.3 percentage point reduction in youth vaping four years after implementation. Retailers in affected jurisdictions typically shift inventory toward tobacco and menthol variants to maintain sales volume.

What are multi-flavor high-capacity devices?

These are devices offering 60,000 to 150,000 puffs with multiple independent flavor tanks in a single unit. They allow consumers to switch flavors without buying separate hardware and are designed in part to navigate pod-specific regulations.

How should retailers choose which flavor variants to stock?

Retailers perform best with a curated selection of fruit-led and ice-finished profiles rather than the broadest possible assortment. Sell-through velocity data from the first 30 days of a new SKU predicts long-term performance more accurately than supplier volume projections.